Inspired by Wobbles. I decided to try out a high-yield online savings account. 2.45% interest with zero fees and minimal hoops to jump through. A few other changes as well. Any pros want to double-check my thought process to make sure I’m doing things correctly?

Previously I had three accounts, all through my local credit union.

A) checking account with 4.00% interest up to $500 and then .05% interest past $500.

B) savings account with 6.00% interest up to $500 and then 0.10% interest past $500.

C) second savings account 0.10% interest.

The way I used them was to put all deposits into checking, all expenditure was put on whatever credit cards would earn me the best rewards for any given purchase, and I’d use the checking account to pay off the credit cards in full before the end of the billing cycle. Saving accounts weren’t used at all.

Now I’ve greatly enjoyed learning how to maximize credit card rewards this past year, and I figured it was about time to do the same with my liquid assets as well. Seems like I’ve been leaving a good amount of money on the table.

So... I opened an online-only high-yield saving account with CIT Bank, which is offering 2.45% interest if you either have >$25,000 in the account (lol, someday) or... If you deposit at least $100 a month. IfIyou don’t meet either of those requirements, the interest rate drops down to 1.04% or something, but depositing $100+ a month shouldn’t be a problem so I can effectively count on the higher rate.

So my current accounts are as follows:

1) Credit union checking account with 4.00% interest up to $500 and then 0.05% interest past that.

2) Credit union saving account with 6.00% interest up to $500 and then 0.10% interest past that.

3) CIT Savings Builder account with flat 2.45% interest assuming I deposit a minimum of $100 per month.

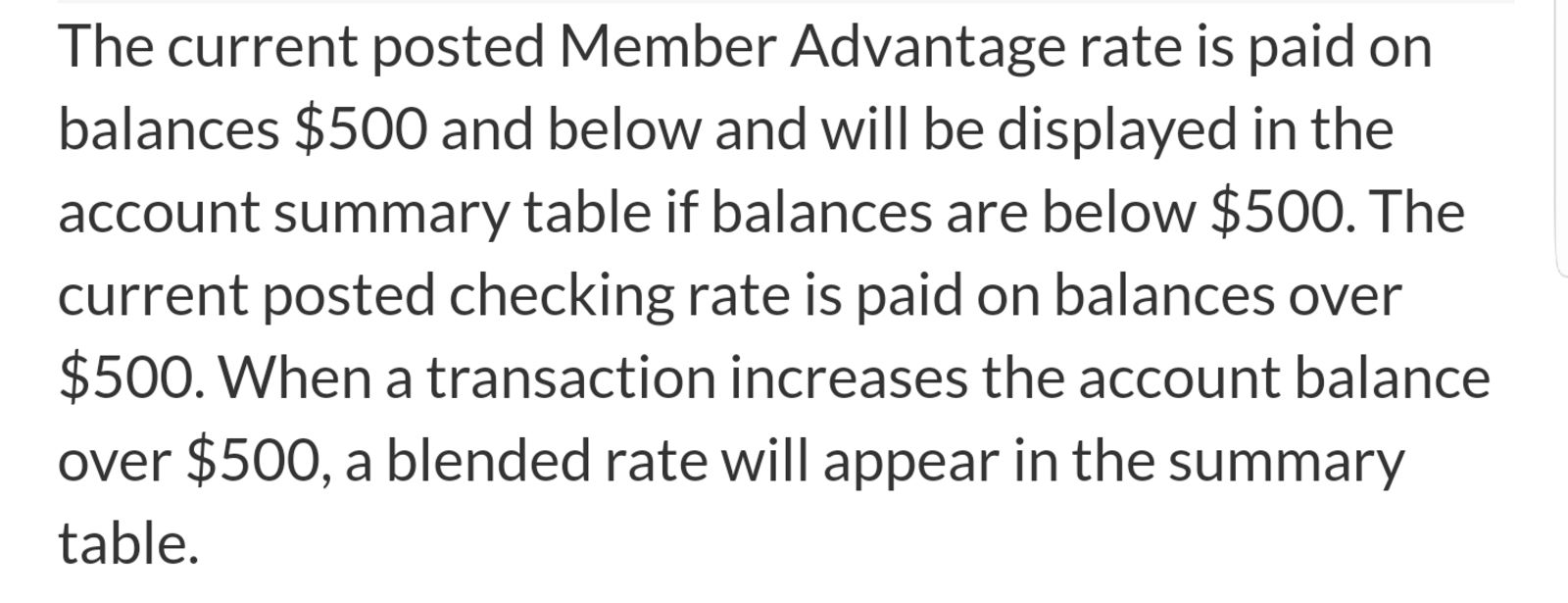

What I’m trying to figure out now is what the best way to divide my money is. One thing I’m not positive about is how the interest rate works when I pass the $500 threshold on the credit union accounts. Do I get the high rate on the first $500 and the low rate on anything past that, or is it that once I’m past $500 in the account I get the low rate for the entirety of the account? The snippet below makes me think I get the good rate on the first $500 every month, even if the total balance goes above that.

More importantly... Does it even matter?

Tell me if this makes sense. I’m thinking I keep $464.00 in the credit union saving account and $480.00 in the credit union checking account each month, and combined earn $56.00 in interest each month, bringing the total balance of each account to $500.00. As soon as I hit the $500 mark, I transfer the total interest earned into the CIT account as it has the highest interest rate for balances over $500. And I just repeat this every month. I can set up some automatic transfers so it’s all automated.

Am I missing something, or does that seem like the way to go?